Table of contents:

Largest Fintech Companies In Usa – Fintech is a mix of finance and technology and is a broad sector consisting of organizations that use new technology in the financial sector. Fintech companies create innovative digital payment processing solutions and design and manage person-to-person payment applications. One of the most searched queries in fintech is “What are the largest FinTech companies by market cap?” »

The market value of a company reveals its value. Metrics serve several purposes; Among other things, understanding a company’s size can help investors make better business decisions.

Largest Fintech Companies In Usa

This is very important to investors because it shows what stock analysts think about the company. In other words, Wall Street uses market capitalization to determine the value of publicly traded companies. This is a big problem because most new investors look at a company’s share price to determine its quality.

Fintechs, You Are Not A Super-app; The 10 Biggest Fintech Companies In America 2023; Open Finance: The Opportunity To Support Small Businesses;

Uninformed investors believe that the higher the share price, the better. It makes no sense to make business decisions based solely on stock prices. Instead, investors will use its market capitalization to estimate its value. Investors look for bargains by looking at a company’s market capitalization.

The fintech sector is one of the most competitive industries in business, whether you are an entrepreneur or not.

It covers the entire spectrum, from capital markets to insurance and digital banking to wealth management. Here are some of the largest FinTech companies in the world by market capitalization.

Visa Inc. is one of the two largest payment card issuers in the world. It had approximately 14,200 employees in 2016. It is a robust global processing network that processes over 65,000 transactions every second, sending safe and secure payments around the world. The company’s constant focus on new ideas is a big part of its promise of a cashless future for everyone, everywhere. Visa has a market cap of $448.13 billion as of January 2022, which is a lot of money.

Startup Industries & Verticals: Key Insights From 2022 To 2023

Mastercard is a publicly traded payment services company headquartered in Purchase, New York, with more than 18,600 employees worldwide. In addition to Visa and MasterCard, these two companies offer payment cards. World: Mastercard is one of them (credit cards, debit cards and prepaid cards). Mastercard’s market cap as of January 2022 is $344.41 billion.

Ant Financial or Alipay is also known as Ant Group or Ant Financial as part of the Alibaba Group. Ant’s platform business strategy is integral to the company’s future success. Alipay is the core of this business strategy. Alipay is similar to PayPal in that it allows two people to make payments to each other. It doesn’t matter if they are consumers, small businesses, domestic workers or people working on the street.

With more than 700 million active users and more than $8 trillion in transactions, Alipay has grown significantly since its inception in 2009. As of January 2022, Ant Financial had a market capitalization of $303.05 billion. By 2022, Ant Financial’s market capitalization will reach $313 billion.

A company’s market capitalization determines how much it can afford. Although a large market cap has some advantages, money is crucial. People want to invest their money in businesses that have the potential to thrive and grow. By clicking Continue to register or log in, you agree to the Terms of Service, Privacy Policy and Cookie Policy.

Top 200 Fintech Companies Revolutionizing The World Of Finance

True super apps like WeChat, Kakao and PayTM, apart from financial management, offer a variety of services across various industries and generally do not dominate banks with an “anchor” product or service. Non-bank apps or ecosystems, especially Apple, seem stronger than ever to bring a super app to the West and there are many reasons preventing fintech from being a super app.

In Europe and the West, many fintech companies claim to be a “super-app” by adding complementary financial or financial management features to their platforms or applications.

One of the closest fintech super apps in Europe is Revolut, which offers partnerships with Stays, VRBO and Experian, enabling Revolut customers to book travel directly within the app. Last year she announced the launch of “Cats”. However, the chat function seems to be only associated with transferring money to a contact. This begs the question: is it a messaging app or an advanced two-way SEO feature when you send money to someone else?

If we look at the big super apps, except for WeChat Pay and Kakao Pay, the flagship service or flagship super app almost always started in the non-financial services space behind it. Alipay and PayTM started as digital wallets for online payments and mobile phone balances, with Grab, UberUBER and Gojek as ride-request apps. The drive to enter the financial services sector was born after adapting their flagship offering to the product market of their respective sectors.

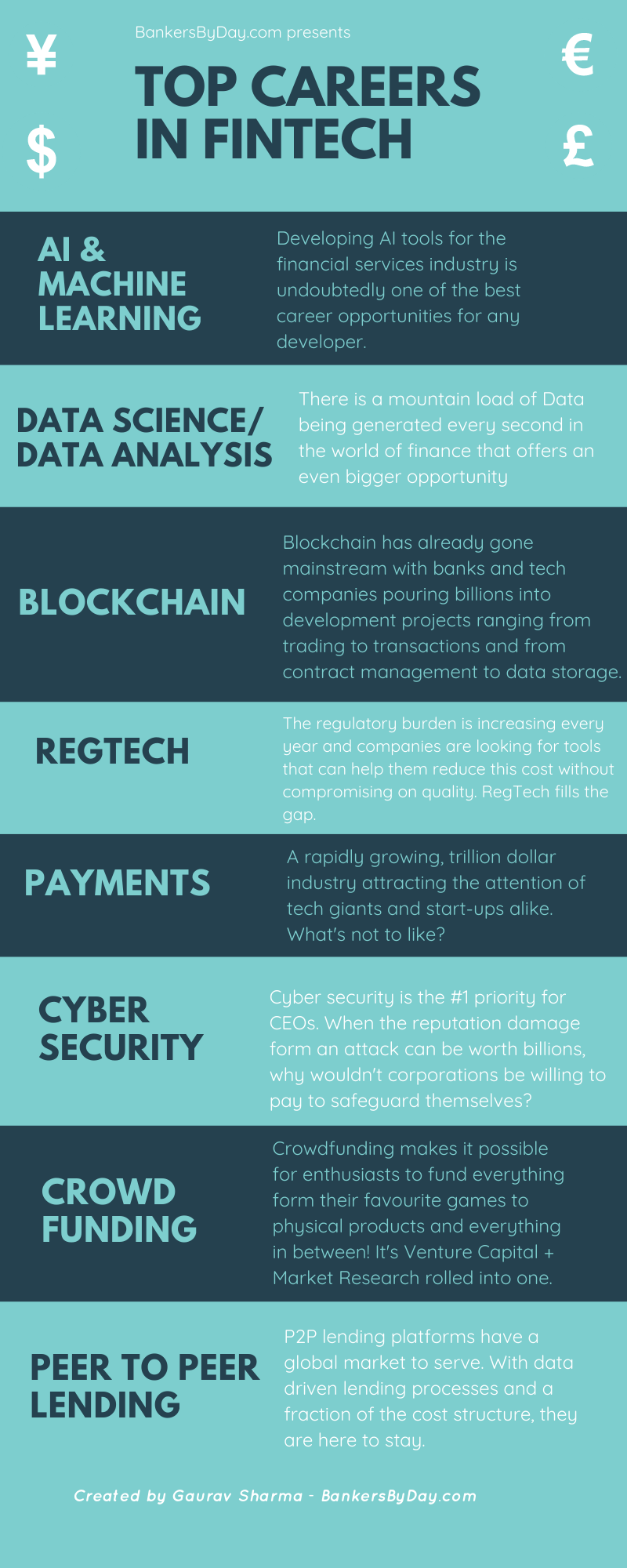

A Complete Guide To Careers In Fintech (2024)

Another key aspect of Super App is the user experience, which clearly allows users to access different services and features without switching between multiple apps.

History has proven that offering an integrated, integrated user experience with a third-party product in a fintech application creates a financial services market that is more than just a super application. In some cases, this strategy has failed.

For example, early in N26’s product offering, it partnered with other fintechs to offer a comprehensive financial management solution such as TransferWise (now Wise) for international payments, Clark for insurance and AuxMoney for loans. However, the problem here was that existing Clark users had to open new accounts under “N26 Insurance”, while Wise users could not use their existing credentials in the N26 app. It’s just a white label to create a marketplace, users still need to run some apps.

As the fintech revolution continues, businesses need to be honest with themselves and their customers about their capabilities and the reach of their platforms. While there is no shame in developing banking as a services platform or focusing on creating a financial services marketplace, it is imperative to avoid prematurely labeling these offerings as super apps.

Analysis: Fintechs Dominate ‘top 30 Digital Islamic Economy Startups’ List

As part of this new partnership, any Amazon Pay merchant in the United States can now choose to offer their customers a “buy now, pay later” option using Affirm’s technology. Merchants who offer Amazon Pay are not required to integrate Affirm as their only premium option. Instead, they can add it to their existing Amazon Pay button.

Affirm first announced a debut partnership with Amazon in August 2021, which was exclusive until January 2023. It began with a launch in the United States before launching Amazon .ca and the Amazon mobile app in Canada.

Now, through what Affirm describes as its Adaptive Checkout technology, the company says it will offer its customers personalized payment options, such as weekly and monthly, starting at 0% APR on purchases over $50. Amazon Pay customers who Affirm as ‘ choose a payment option must first be approved in a process that Affirm says will not affect their credit scores.

The fintech company has consistently claimed that customers using its technology “never pay more than they agree to” because “there are no late or hidden fees with Affirm.”

Building Momentum: Me Fintech

For consumers, this is another way to spread payment for their purchases. Amazon Pay generally makes it easier for users to order items online without entering their name, address and payment information, as it allows them to log into their accounts with just one click. For retailers, this convenience is already more likely to translate into increased sales, and presumably more payment options will only boost sales. Additionally, Affirm says that retailers who offer Amazon Pay with Affirm will be able to access a new shopper network now that 16 million shoppers “actively use affirm.”

To confirm, the agreement represents a scale of the existing relationship between the two companies. Currently, Affirm is already used by “millions” of customers in the United States and Canada on Amazon.com and the Amazon app.

Open finance can improve open banking standards and practices in ways that encourage innovation and competition among small businesses, as well as participation and data sharing.

Small businesses are looking to policymakers and regulators to develop solutions for small business-specific data sharing with easy access to standard APIs and support from third-party providers.

Atlanta’s Fintech Landscape

A number of questions will need to be answered to unlock the opportunities that Open Finance can offer:

The potential of open banking for small businesses has not yet been fully realized and should be a major priority.

Access to finance: There is currently a significant financing gap for small businesses. Open finance will benefit these businesses, which will be more likely to obtain affordable credit and benefit from a more efficient application process. It will support borrowers, help them create personalized products and make quick decisions through improved credit screening processes.

Cash flow management: Small businesses struggle to predict their cash flow and cash flow based financing is on the rise. Open Finance can make cash flow-based invoicing and forecasting more accurate and personalized.

Fintech Startups In Philippines

We assume that payment companies generate their revenue by processing transactions. However, companies can generate revenue from a variety of sources.

Appeal